| Search for content and authors |

A method to estimate company performance using global inter-firm relationships |

| Takayuki Mizuno |

|

National Institute of Informatics, Tokyo 101-8430, Japan |

| Abstract |

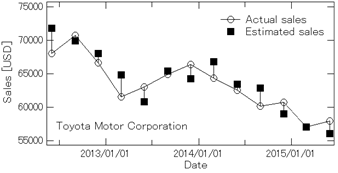

In economics and finance, asset price bubbles are defined as the deviation of the price of an asset from its fundamental value. The main factor of company’s fundamentals is financial variables. However, it is not easy to always obtain information about financial variables. The financial variables are discretely published quarterly as settled-account reports, whereas, stock prices change at speeds of one hundredth of a second in the stock market. In order to measure gap between asset price and fundamentals, we must always nowcast company performance in the time between one settlement report and the next. In this paper, we establish an estimation method of financial variables with high estimation accuracy by using global inter-firm relationships. There are many companies with similar business, sales area and sizes in the world. The companies have business connections. Because the settlement dates are different for many companies, we may estimate unreported financial variable of each company from already reported financial variable of similar companies. We investigate whether it can be estimated using a unique dataset that covers list of business connections and a highly structured companies’ revenues by geographic and business segments. Through the analysis of random forests, we found that common shocks affected by each company can be measured from revenues of companies that operate in the same area. This result means that the main component of common shocks is foreign exchange fluctuations. We also can estimate individual shocks of each company from the revenue fluctuations of suppliers and customers because there is shock propagation through business connections [1]. Fig. 1 shows Toyota’s sales estimated by this method. The estimation accuracy is sufficiently high. In this conference, we will report these results and discuss the estimation accuracy compared to I/B/E/S data that includes empirical estimates by many economists and analysts. Furthermore, by also estimating I/B/E/S data with this method, we clarify what kind of information changes their estimates. Such analysis is important from the viewpoint of agent-based modeling of financial markets.

Fig. 1 Estimated Toyota's sales. [1] T. Mizuno, et al. (2014) The Structure and Evolution of Buyer-Supplier Networks, PLOS ONE 9, e100712. |

| Legal notice |

|

Presentation: Oral at Econophysics Colloquium 2017, Symposium C, by Takayuki MizunoSee On-line Journal of Econophysics Colloquium 2017 Submitted: 2017-03-16 09:45 Revised: 2017-03-16 10:32 |